IKIGAI DECISIONS IN WEALTH MANAGEMENT

The Realities of Life

In the hustle and bustle of daily life, it is easy to become consumed by routine tasks and life’s obligations. Carving out moments for introspection is challenging while juggling work, family, and a myriad of other demands.

Calling it “being caught in the rat race” may seem a bit harsh, but it is a reality many of us face. The constant pressure to succeed and keep up with others can create a never-ending cycle of busyness, leaving little room for reflection.

So, if we would like to consider what truly defines a good life—where do we even start? Does having more money in our pockets equate to living a good life?

Mindsets on Living a Good Life:

YOLO Versus Fire

YOLO Versus Fire

The popular ‘You Only Live Once’ (YOLO) ideology often encourages people to spend most of their financial surpluses today, over saving towards a future goal.

The danger of this mindset is that when you realise the need to begin saving for your future, it may occur at a much later stage. By that time, you may need to invest in much riskier products to achieve your goals. With that, there is also a higher risk of not being able to reach your goals, with the stress seeping into your health, relationships, and career.

Surely, a good life is more than just buying that branded Chanel bag or driving that latest Tesla car, although there is absolutely nothing wrong with that. But are we simply buying things that we do not need, with the money that we do not have, just to impress the people who do not care? The YOLO mindset makes you a servant to money when it is merely a tool towards achieving your life goals.

Conversely, the ‘Financial Independence, Retire Early’ (FIRE) ideology promotes extreme saving, careful spending, and early retirement. While FIRE can lead to financial freedom, it also means sacrificing your current enjoyment, potentially straining your mental health and relationships.

Life is uncertain, and although the FIRE mindset sounds prudent in planning for tomorrow, it assumes there will be a tomorrow—something no one can know for sure. The only certainty in life is that we will all die someday.

Ikigai Decisions:

Your Non-Negotiable Life Goals

Your Non-Negotiable Life Goals

Gleaning wisdom from the drawbacks of both YOLO and FIRE ideologies is what Providend terms the ‘Philosophy of Contentment’ or the ‘Philosophy of Sufficiency,’ established since 2010, where you actively pursue what is most important for you in life. You will be at peace, knowing that although you cannot have everything in life, you have clarity on what you must do in your lifetime.

We believe that with awareness of what you must do, it is the beginning of your journey towards Ikigai-kan (生きがい感 in Japanese)—the feeling of a life that is worth living.

Our Founder and CEO, Christopher Tan, has explained in this article, the true meaning behind the word Ikigai and how it has been greatly misrepresented in a four-circle Venn diagram. Rather than Ikigai being “a reason for being”, it is the “deciding of things that are most important” life decisions, also termed as Ikigai decisions.

By making Ikigai decisions, we help our clients reach a state of restfulness, allowing them to pursue what is most important to them in life today, while concurrently preparing for their future.

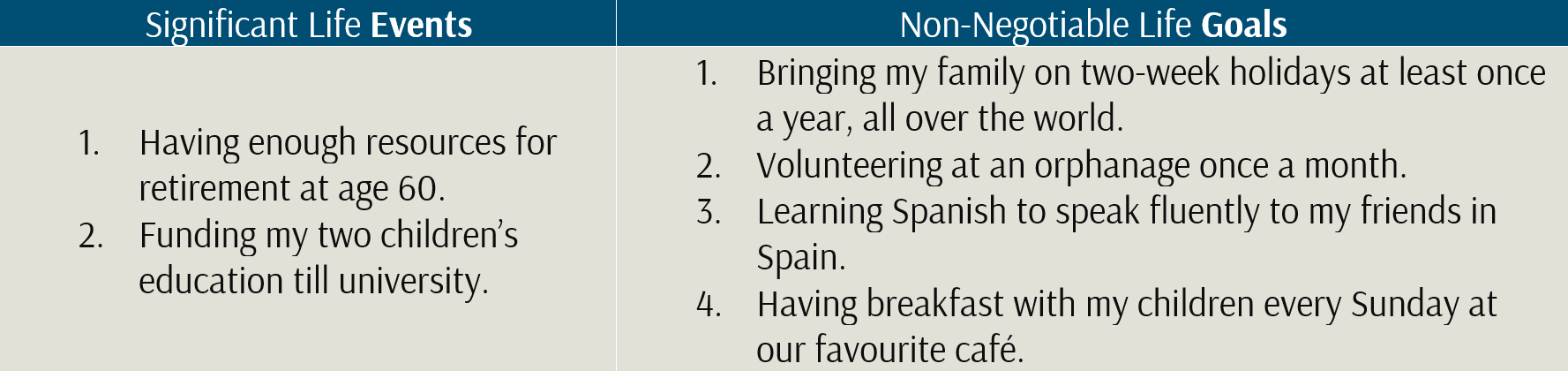

In the book, Repacking Your Bags, authors Richard J. Leider and David A. Shapiro defined the good life as “living in the place you belong, with people you love, doing the right work, on purpose” and through deep conversations with our Client Advisers, we seek to find what the good life means for our clients by uncovering both their significant life events and non-negotiable life goals.

What is the difference? Here is an example:

Figure 1: The Difference Between Significant Life Events and Non-negotiable Life Goals

At Providend, we believe you should first make life (Ikigai) decisions, and only then consider the financial decisions to enable your Ikigai decisions.

PROVIDEND’S APPROACH

Seeking the Highest Probability of Success for Our Clients.

Our clients’ Ikigai decisions are of deep importance to us, and our Philosophy of Contentment guides Providend’s company policies, our strong corporate culture, and our methodology for our clients’ wealth plans. This is why clients and observers alike have described us not only as their wealth advisers but also as their trusted friend and guide, always putting their best interests at heart.

Our approach is to help our clients attain the highest probability of success towards reaching both their significant life events and non-negotiable life goals. This approach requires the wealth planning process for each client to be thorough, holistic, and comprehensive, supported by an experienced team of experts in their respective fields.

This Philosophy of Contentment is expressed through Providend’s six wealth solutions and the way we guide our clients through their Ikigai decisions.

ONE

We have deep conversations with you to uncover your non-negotiable life goals and develop a comprehensive wealth plan to achieve them. There will be ongoing dialogue to adjust your wealth plan according to your evolving needs, market fluctuations, and economic changes.

TWO

We provide you with a positive investment experience and enough returns for you to achieve your goals reliably. We do not seek to maximise returns for you to go through an emotional rollercoaster for money that you do not need for your life goals. Because at this point, you would already be quite clear on your Ikigai decisions. We may even suggest investing less in the markets and using a portion of your money to take your family on that two-week holiday—an investment in your family.

THREE

We review and customise an insurance plan to cover exactly what you need while minimising your costs and avoiding being over-insured. This means you can allocate any insurance savings towards your investments and life goals.

FOUR

With contentment and celebrating your life in mind, we help you document how you want your loved ones to know how to care for you, in the case of an unfortunate medical crisis impairing your capacity to make decisions. We also help you express your true intentions of distributing your financial assets upon your demise, protecting your family’s harmony, while leaving behind your valuable legacy.

FIVE

Whether business owners like it or not, you will have to exit your business one day whether due to death, poor health, or retirement. We will help you develop a customised business exit strategy that enhances your business’s value and integrate it with your personal wealth plan.

SIX

Using our proprietary RetireWell™ methodology, we will design a retirement income plan that provides you with a reliable stream of income for the rest of your life. This way, you can retire with peace of mind, with enough resources for your retirement by age 60, as illustrated in the “Significant Life Events” example above.

Conflict-Free

Wealth Advice

Wealth Advice

In this video, our Founder and CEO, Christopher Tan, talks about the importance of conflict-free wealth advice that is holistic, instead of advice that is piecemeal or product-focused. He also shared about Providend being an institutionalised firm and the importance of a team approach in wealth advisory, because no one person can be an expert in every area.

The Restfulness of Life & Your Ikigai-Kan

Being a trusted adviser to our clients for over two decades and managing in excess of $1 billion worth of their hard-earned money, we know the importance of reliability and sufficiency of investment returns to meet their significant life events and non-negotiable life goals.